- Valuation Model

- Expert Interviews

- Founders, funding

What does the competitive landscape of the second-hand clothing market look like?

Marcelo Ballvé

Head of Research at Sacra

We completed a high-level survey of competitors in the second-hand clothing (SHC) market to gauge basic trends and identify benchmark companies. For the scope of this request we focused on extracting headline figures and metrics, alongside macro competitive trends. Future research might drill in on certain themes and companies, andmore granular metrics.

- Identifying significant competitors to Charity Shoes and Clothing, LLC

- Collecting indicators of scale including volume of clothing processed, warehouse space, and employees. In many cases, this data is available on company materials, social media, and websites, as well as media coverage and trade publications.

- Broad competitive trends are likely to impact the market for SHC in the near future, including the rise of Asian suppliers, the vertical integration of buyers (e.g. Megapaca), and demand growth in the developing world.

- Expanding color and context from the data dossier that will follow up this deliverable, e.g. recent warehouse expansions and the establishing of multinational and multi-vertical operations as a norm for large players in this industry.

A handful of companies are clearly setting the pace in what remains a fragmented market. Meanwhile as a whole, the industry is confronting accelerating trends that are likely to impact competitiveness and margins in the next three to five years.

These accelerating trends include:

- Nascent consolidation, alongside multinational expansion of supply and logistics chains to rationalize costs.

- Increasing automation. Along with nascent consolidation, this trend puts pressure on smaller-scale companies who will increasingly be at a disadvantage from larger players’ gains in scale

- Pressure from Asian suppliers, especially in China.

- Increasing importer leverage, which is in part a result of increasing volumes from exporters in Asia, but also importers’ own vertical integration and efforts at scale (e.g. Megapaca in Central America).

Competitive landscape: structure of the SHC reuse and export market

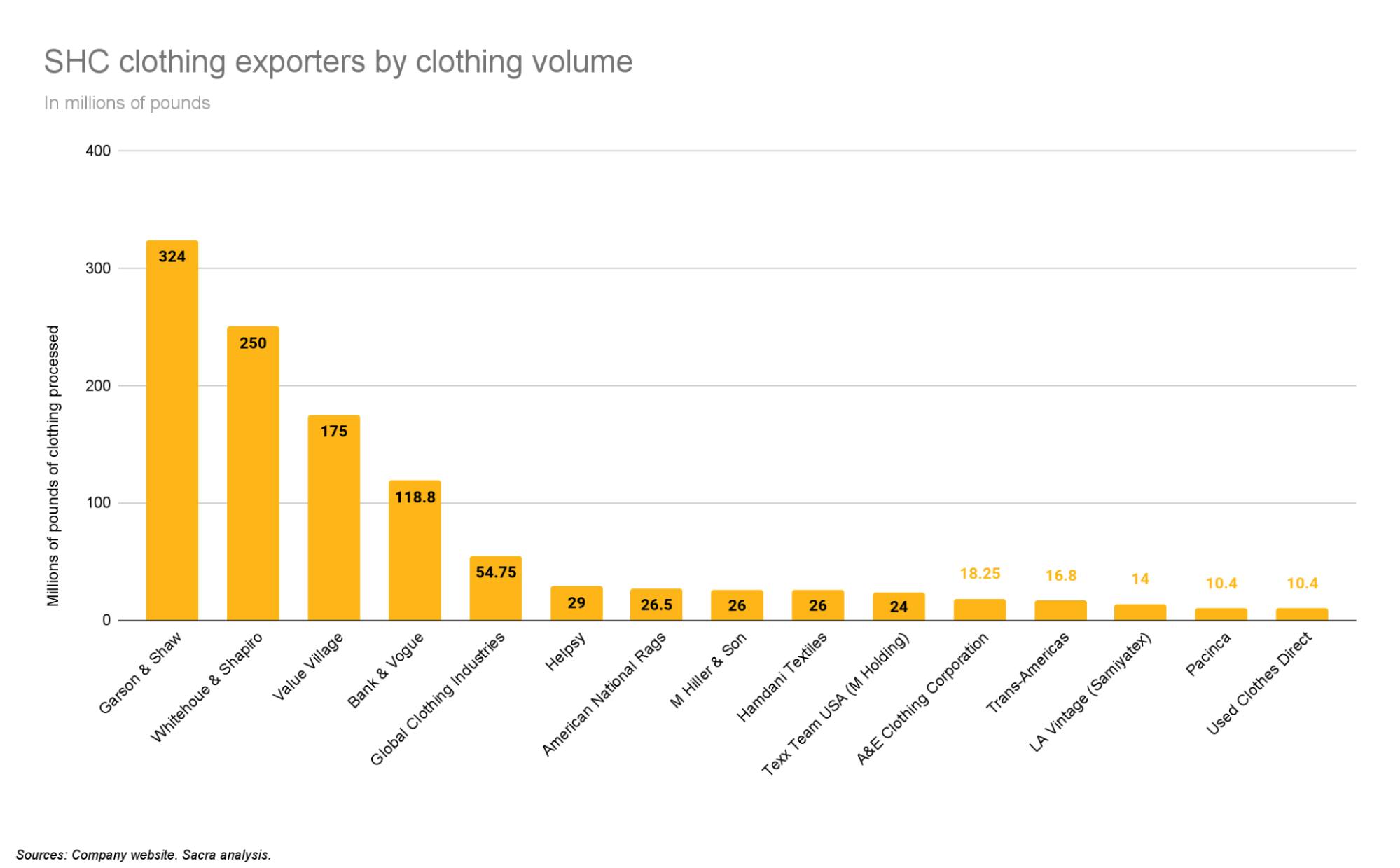

A possible categorization of this market is by the scale of SHC suppliers seen through the lens of clothing-processing volume. A clear distinction in this market can be drawn according to the cumulative weight of clothes processed annually by each supplier (see chart, below).

Classifying SHC suppliers by processing volume

As seen in the chart above, the resulting market structure reveals a handful of suppliers that have meaningful scale. We define these “Scalers” as SHC operations that are processing 100 million or more pounds of used clothing per year.

Beyond these companies there are two subscale categories, those we call “Contenders,” which are processing 50 million or more pounds annually, and “Strivers,” which are processing between 10 million and 49 million pounds of clothing per year. Finally, there is a considerable long-tail of laggards, i.e. suppliers that process less than 10 million pounds of clothing.

- Scalers: +100 million pounds

- There are four companies identified in this category: Garson & Shaw, Savers Value Village, Whitehouse & Schapiro, and Bank & Vogue

- Contenders: 50 million to 99 million pounds

- We only identified a single company in this segment of the market: GCI

- Strivers: 10 million to 49 million pounds

- There are 10 in this category, Helpsy, American National Rags, M Hiller & Sons, Hamdani Textiles, Texx Team USA, A&E Clothing, Trans-Americas, LA Vintage (Samiyatex), Used Clothes Direct, and Pacinca

- Laggards: Up to 9 million pounds

- There are likely hundreds or even 1000s of firms in the long-tail of this market in the US and Canada.

There are suppliers that fall outside this classification because they operate solely as intermediaries. Their arbitrage is to buy large weights of used clothing and further take advantage of their cost-advantaged lightweight operations — i.e. lack of warehouses, equipment, and staff — to price their clothing at a modest mark-up. Thus, they achieve a niche in the market despite having to source from wholesalers themselves. Some are specialists — they curate according to suppliers, geographies, or grades — and lean into sourcing niches in order to achieve a desirable balance between quantity and quality.

Other characteristics: workforce, warehouse foot-print, revenue streams, and retail operations

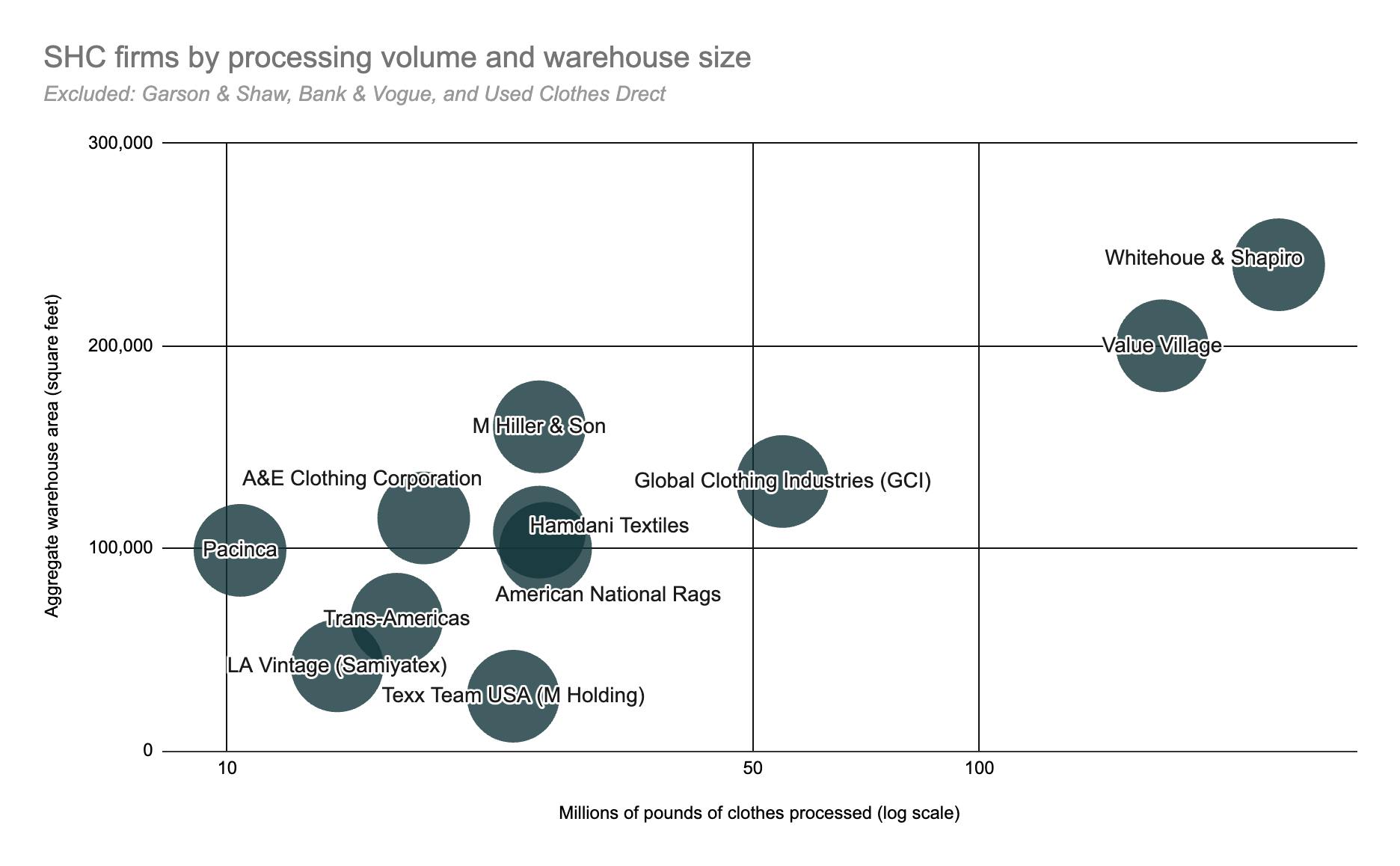

The above four classifications of SHC suppliers — Scalers, Contenders, Strivers, and Laggards — manifest other characteristics that are tied to their relative volumes of clothes processing.

One such metric is the number of employees; clothes sorting and grading operations require manual labor. That said, there is equipment that can automate or speed some of this work, including automated balers, conveyors, etc.

Another is the size — in terms of area — of the facilities that are able to house the sorting and storage operations. As can be seen in the chart above, total warehouse floor space correlates positively with the volume of clothing processed annually. Firms handling larger volumes have a larger real estate footprint.

This is somewhat obvious, as clothing is bulky and somewhat prone to deterioration. Processing it requires relatively large, roofed, and moisture- and temperature-controlled areas. Whitehouse & Schapiro in the Baltimore area, and Savers Value Village in Canada are two firms that have aggregate warehouse space of 200,000 square feet or more, according to company websites and media coverage.

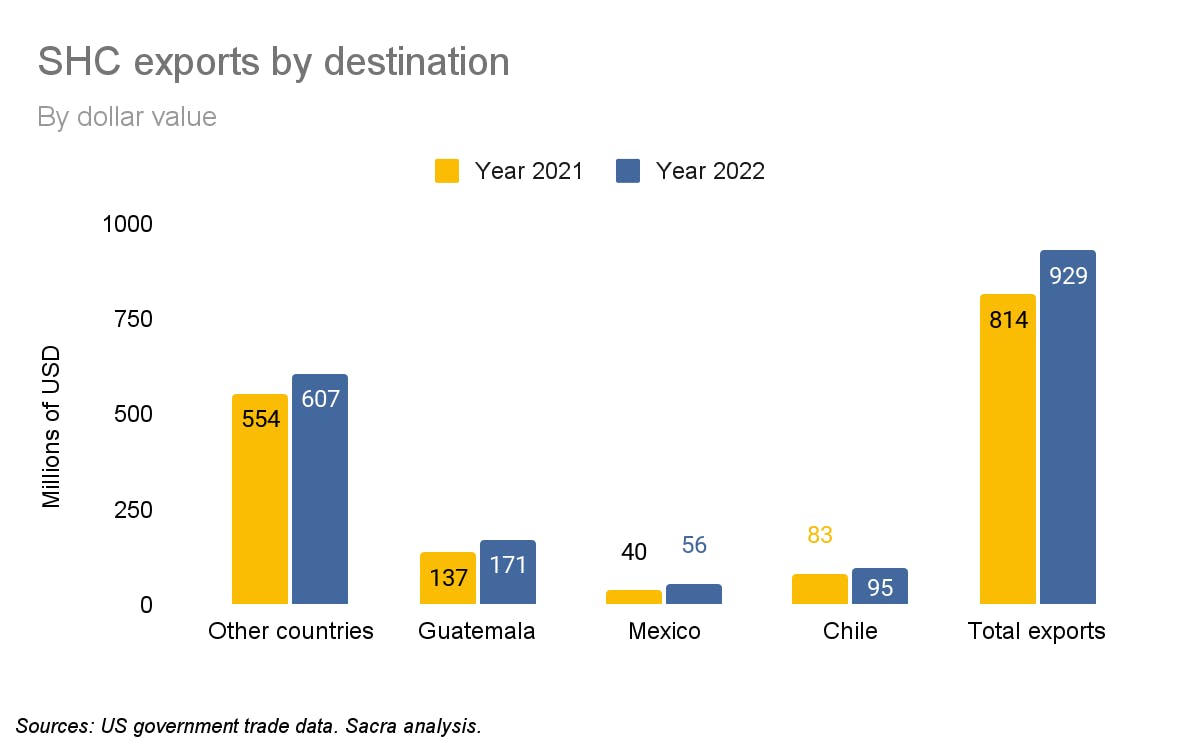

Growth in export markets

Between 2021 and 2022, US used clothing exports grew by 14%, to $929 million, on track to break the $1B mark in 2023, according to US government trade data. Exports to Mexico and Chile grew by 40% and 25%, respectively.

US exports grew more quickly from 2020 to 2021, when they expanded by some 35%, according to the OEC, but that may be a post-COVID bump.

The percentage increase in export growth is likely a more accurate representation of industry growth overall than broad-based numbers on the textile-recycling, secondhand clothing, and thrift industries. They are a more accurate reflection of the revenue pool tied to exporting SHC clothing in bulk, while other figures tend to include other revenue streams tied to manufacturing, retail, and textile reuse domestically.

Revenue streams

Many of the firms that sort and process used clothing will have several streams of revenue.

- Wholesale clothes: They will resell used clothing on a wholesale basis to local intermediaries and importers in developing countries

- Wholesale rags: Supply firms domestically or overseas that process discarded textiles, i.e. “rags,” into dish or wiping towels,

- Textile primitives: Clothing that is no longer usable as such can also be processed into textile-based primitives that can be upcycled into new products.

- Retail: The largest and most sophisticated firms will have other revenue streams as well, including retail: for example, LA Vintage/Samiyatex and Bank & Vogue operate chains of thrift stores in which the highest-quality and commercializable items can be sold at retail prices.

The prices for export-worthy reusable clothing is at least 4x higher than that for degraded or dirty clothes used for rags or other upcycling. So, smart sourcing, alongside efficient and effective sorting, are meaningful in stewarding revenue quality.

Competitive trends in summary

- Nascent consolidation

- Pressure from Asian suppliers

- Increasing automation

- Increasing importer leverage

A full treatment of these trends is beyond the scope of this memo, but example “mini cases” can make the points clear and crystallize the potential impacts of these trends.

Nascent consolidation

Consolidation and efforts to leverage scale are beginning to push through this industry. Larger firms are acquiring smaller SHC exporters or effecting expansions in search of scale and better margins. Some examples:

- In 2021, Savers Value Village acquired a stand-alone SHC thrift business, 2nd Ave., which has $7.95 million in wholesale SHC revenue, as shown in Savers Value Village S-1. Savers Value Village was itself owned by Ares Management Corp. and completed its IPO in early 2023.

- Bulgaria-based Texx Team has expanded aggressively in the United States, with two units that are held within an umbrella company, M. Holding.

- In 2012, the group launched Green Team Worldwide, which specializes in collecting clothes in the US and Canada, and has thousands of collection bins across North America. Today it has warehouses in urban centers, including Vancouver, Los Angeles, San Francisco, and Seattle. In 2017 alone, Green team collected 22 million pounds of clothing in North America. These are processed for sale or export by Texx Team USA (see below). According to the company, “Green team Worldwide Environmental Group is in the process of constant expansion, as the main long-term goal is to cover all the states of USA and Canada.”

- In 2017, Texx Team USA opened a warehouse in New Jersey to anchor its SHC operations in the US, which also imports clothing from Europe and elsewhere.

- Bank & Vogue has steadily grown its footprint of textile recycling and manufacturing businesses and retail operations (Beyond Retro vintage retailer), which include a textile manufacturing plant in India specializing in upcycling discarded, unusable textiles into new textile products. In 2020, it signed a multiyear agreement to supply up to 30,000 tons of textiles to Swedish textile recycler, Renewcell, which manufactures the Circulose-brand fabric created from pre- and post-consumer textile waste.

- Whitehouse & Schapiro acquired a new 80,000 square foot warehouse in Rosedale, Maryland early in 2023, to support operations at an also recently acquired 164,000 square-foot facility in 2019 in Hanover, MD. Media reports state that the new operation complements their existing facility, but further confirmation should be sought.

Pressure from Asian suppliers

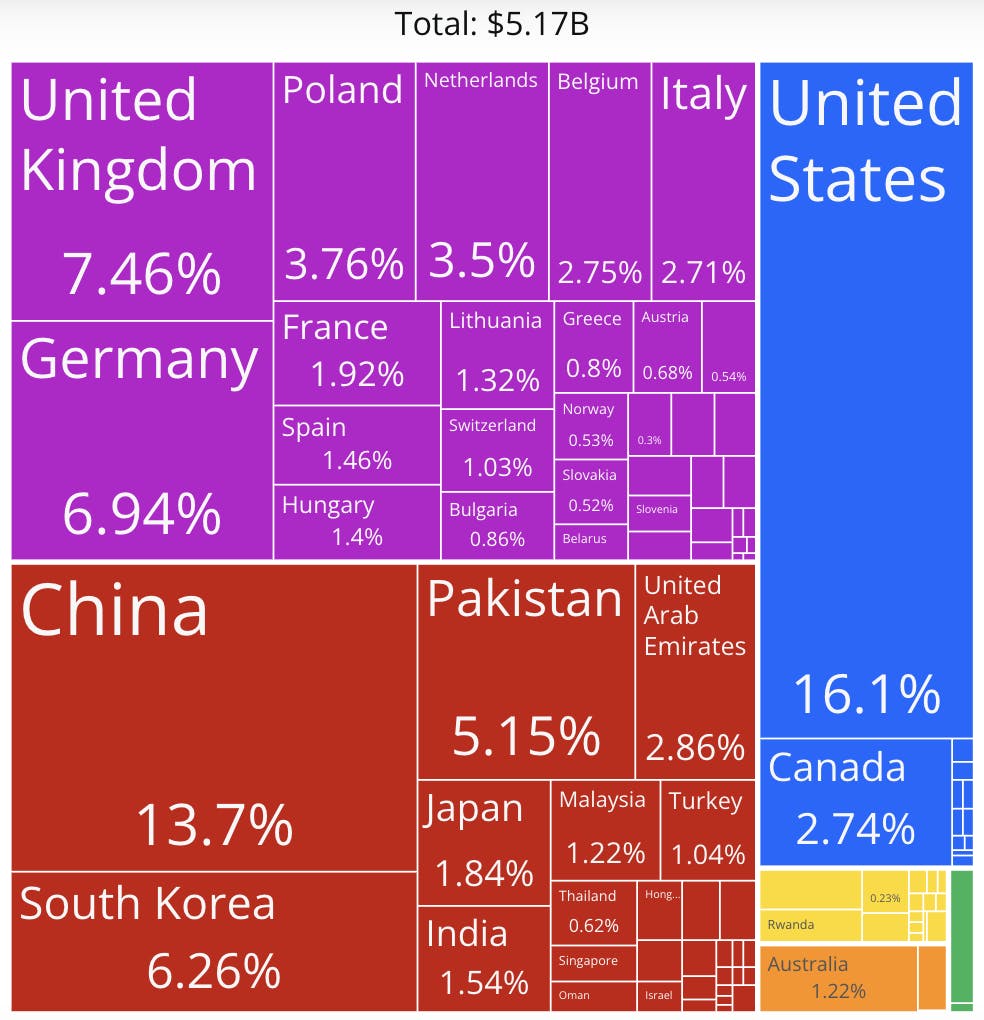

China is emerging as a major exporter of SHC, particularly to Africa. Chinese exports of SHC are growing more quickly than US exports, having seen 84% growth in export value in 2021, vs. 35% in the US in that year (as already mentioned). The value of Chinese SHC exports have grown in the triple digits in many African markets (164% in Angola between 2020 and 2021).

China was a close second place to the United States in volume of SHC exports in 2021.

China has a 13.7% share of global exports of $5.17 billion in that year (Source: OEC).

- For example, after its founding in 2013, Hissen Global has scaled tremendously on the back of four principal brands, Hissen, Zagumi, Space, and the preexisting Indetexx (Zagumi and Space are Africa-focused). Together, the companies export over $50 million in used clothing globally to 60 markets. The principal facility is a 215,000 square-foot warehouse and processing center, but Hissen has at least nine other major facilities: two additional facilities in China, one in the Philippines, as well as six warehouses in Africa.

The volume handled by Hissen Global, and the increasing prevalence of western-style clothing of consumer quality in China, indicates that it will be able to price competitively in any markets where it competes head to head with US- or Canada-based suppliers.

Increasing automation and technology

New technologies promise to reduce the manpower needs of key stages in the processing and sorting of clothing.

Assembly-line style approaches are already the norm in the industry, as much depends on the accuracy of sorting.

Hamdani Textiles assembly lines for sorting used clothes.

Precision is important for yield. Reusable clothing must be processed into the more expensive for-export bales often classified by the type of clothing (e.g. women’s blouses, “tropical blends” of shorts and T-shirts). These must be set aside from textiles destined for waste, rags, or processing into new products.

A worker at Coleo Recycling in Spain collects clothing pre-sorted by a Picvisa Ecosort Textil unit.

A promising technology in this regard is optical sorting, which is able to automate the processing of clothes by color, shape (garment type), and components (textile material) through a combination of deep learning, computer vision, and spectroscopy. In the latter, NIR or near-infrared technology, is used to detect the fiber content of clothing. This allows for pre-sorting of, say, white cotton T-shirts from garments using polyester and synthetic fibers, and/or garments of other colors and types. It is easy to imagine variations of this technology and applications relevant to for-export used clothing operations.

Increasing importer leverage

The example here is Megapaca, which is gaining leverage both by growing scale regionally (which increases their price-negotiating power), adopting technology, and by expanding up and down the value chain.

- Megapaca, a major used-clothing importer and buyer in Central America, has its own retail operation there, including massive stores of more than 20,000 square feet. Megapaca has announced it plans to compete directly with North American thrift store chains such as Goodwill and Value Village by opening a thrift store chain of its own in the US market. It does not seem far-fetched to imagine that once it does so, Megapaca will take the next logical step and will also launch its own US-based clothing supplier, as Texx Team has done. By vertically integrating, it would cut its reliance on suppliers such as those mentioned in this memo and also improve its margins.