Rohit Kaul

Research at Sacra

Mercury is an online bank for startups. Mercury’s website offers startups a modern UI, fast account approval, and free/low-fee banking products.

Mercury has raised $152M and was valued at $1.6B in its last fundraising round in 2021.

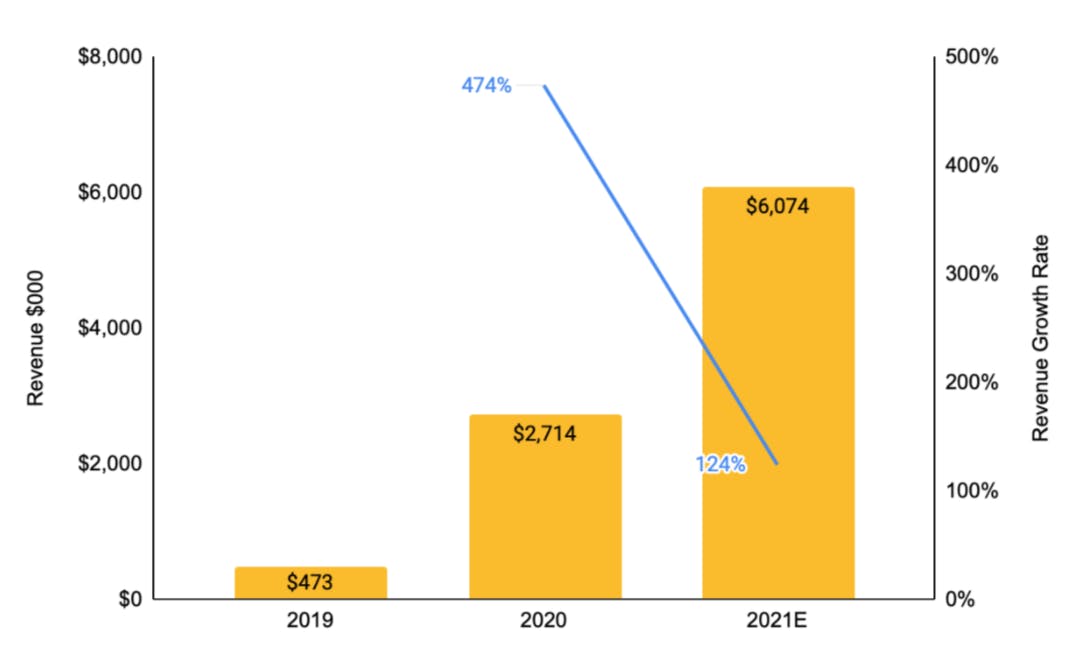

Mercury has 63,000+ customers with an estimated 2021 revenue of $6M. Mercury’s primary revenue sources are:

Revenue from interchange was 94% of total revenue in 2020 and 28% in 2019. The remaining revenue came from rebates. In the future it can earn revenue from interest on customer deposits, interest on term loans, and commission from investment in funds as a part of cash management.

Mercury found product-market fit with early-stage startups by reducing the friction in opening a new bank account. It provides fast online bank account approval without any manual interventions, zero-fee banking products, and a modern UI compared to the legacy UI of existing banks such as SVB.

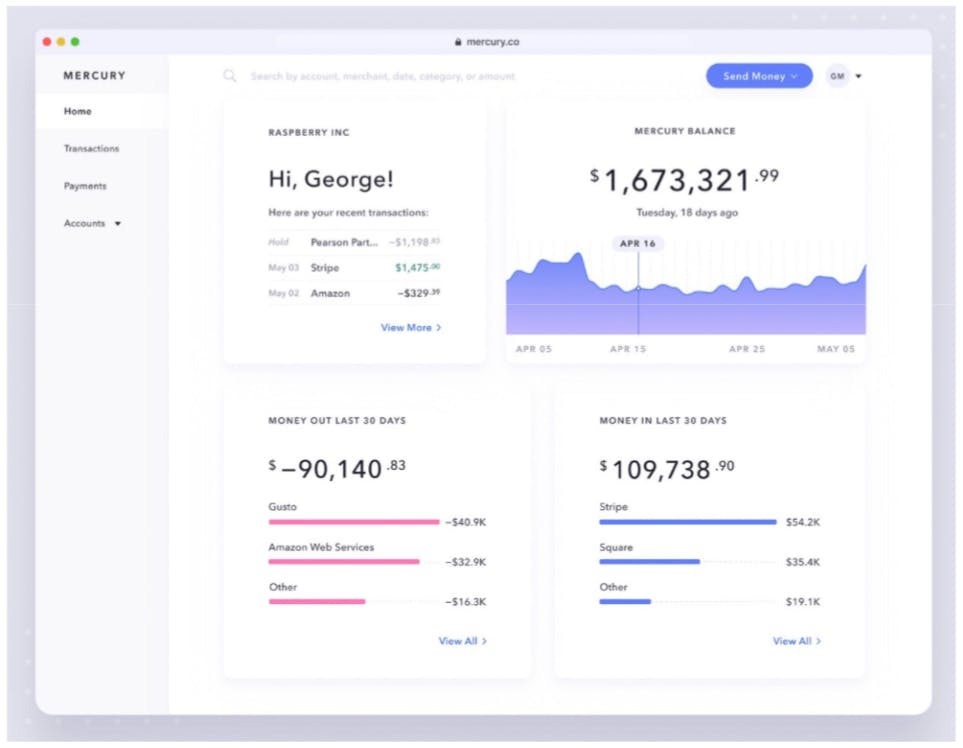

Mercury's dashboard

Mercury offers banking products and venture debt to startups. Its banking products include FDIC-insured saving/checking bank accounts, physical/virtual debit cards, cash management, wire transfers, and banking API access. It recently launched venture debt for VC-backed startups.

Banking products

Mercury’s banking products are free without monthly account maintenance fees, overdraft fees, or wire transfer charges. It offers two pricing tiers (a) Standard, which has no minimum balance requirements and (b) Tea Room, with a minimum $250K deposit that gives access to new products like cash management and dedicated on-call support.

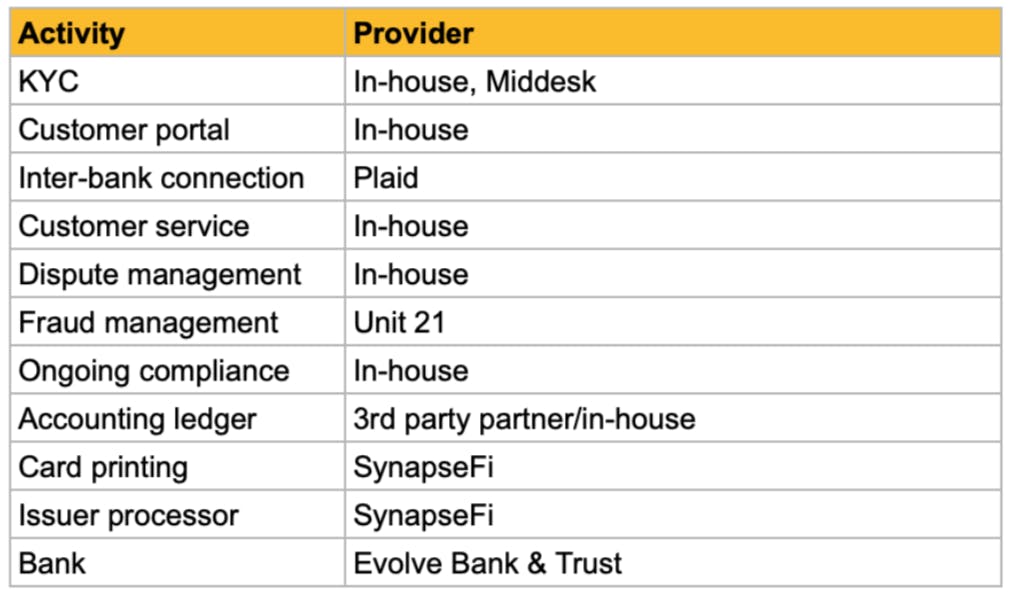

Mercury’s banking stack

Mercury’s UI is designed to reduce time spent doing everyday tasks such as sending money using ACH/money transfer, searching through transactions, and tracking money inflow/outflow. Mercury provides features that fit well with a startup’s digital workflows, such as APIs for bulk/programmatic payments, custom user permissions, and native integrations with payment processors & accounting software.

Mercury uses SynapseFi as the BaaS provider and Evolve Bank and Trust as the charter bank.

Venture debt

Mercury launched its venture-debt product in March 2022. It provides up to 48 months term loans to startups that have already raised $2M+ from institutional investors. Evolve Bank offers the loans, and Mercury monetizes through origination fees and interest (expected to be 4-5%). It also receives a warrant/right to purchase equity in startups' common stock.

Startups can apply for debt through Mercury’s website, submit documents prepared for the earlier VC round and use the funds flexibly for their business goals. Mercury wants to make its venture debt product different by avoiding the spreadsheets & documentation required by banks such as SVB and First Republic.

Ecosystem

Mercury also runs non-monetized community initiatives such as Investor DB and Mercury Raise. Investor DB is a list of seed and pres-seed investors for startups. Mercury Raise is a startup and VC introduction platform.

Mercury needs customers that grow fast and raise a lot of venture capital, allowing it to monetize through deposits/cards. Investor DB and Mercury Raise provide Mercury with direct relationships with high-growth startups that can become future customers. Mercury Raise has worked with 270+ startups and made 1500+ introductions between VCs and Startups.

Startup business banking does not have an established website-based, modern UX startup seen in other areas such as card/expense management (Brex and Ramp), payroll (Gusto and Rippling), or payment processing (Stripe and Adyen). Mercury is trying to own a startup’s first bank account and sell financial services on top of it by providing a completely online, fast, and low fees banking experience.

Mercury is competing against incumbent banks like SVB and First Republic. They are the few legacy banks with the flexibility to work with startups. SVB is used by ~50% of VC-backed tech and Life Sciences companies.

It also competes with fintechs such as Brex, Rho, Relay, and Novo. Brex and Rho used credit cards as a wedge to get into the center of fund flows for startups and are now trying to be all-in-one financial solutions. On the other hand, Relay and Novo are point solution fintechs that provide bank accounts, cards, ACH, and wire transfers to startups, similar to Mercury.

Incumbent banks

Unlike Mercury, SVB and First Republic are full-fledged banks with a combined market cap of ~$63B. Their products can scale with startups as they move from early-stage to late-stage and IPO. Startups/founders get more products by having a direct relationship with these banks that they don’t get from a neobank like Mercury. For instance SVB offers working capital loans, asset management, forex management, and private wealth management.

However, many of SVB’s processes are manual, with time consuming paperwork. They also charge various fees, such as overdraft, monthly account maintenance, and ACH, that early-stage founders find frustrating. Compared to this, Mercury has no monthly fee, no overdraft fee, and free bank accounts that can be managed from its website.

Mercury will need more than a modern UI and fast online account opening to compete with SVB/First Republic at scale. As its customers grow, they will demand more banking products and can churn if Mercury is not able to provide these. To continue to scale, Mercury needs to increase its product velocity to have more banking products.

Fintechs

Fintechs like Brex and Rho are expanding beyond credit cards to control all nonpayroll funds flow through banking, AP, and spend management products. Brex is the largest fintech in this space, valued at $12.3B. Its focus is shifting to late-stage startups/enterprises. Thus it is not directly competing against Mercury for early-stage startups.

Relay and Novo target early-stage startups with free banking products similar to Mercury but have limited features. Relay doesn’t provide savings accounts and term loans. Behind the scenes, it uses Synapse and Evolve Bank, the same as Mercury. Novo doesn’t provide ACH/wire transfers or cash management. Mercury is a more popular brand than Relay or Novo among early-stage startups. Mercury has raised $152.2M compared to $19.4M by Relay and $135M by Novo, which gives it a bit more runway. Mercury has also onboarded some high-growth startups such as Lunchclub, Mighty, linear and Stir.

Brex is a direct, large competitor for Mercury with its Brex Cash product. Brex’s AP and spend management products embed deeper into startups’ workflows than a bank account. Thus, for a startup using Brex, it will be hard to switch to Mercury. Brex has earlier applied and withdrawn its bank charter application. In case it successfully gets a bank charter, it can launch products that out-compete Mercury’s offerings.

Some strong tailwinds in the VC-backed ecosystem support Mercury’s future growth.

Early-stage VC

VC investments in early-stage startups are increasing rapidly. In 2021, VCs invested $84.3B (2X of 2020) in 5,300 early-stage deals (57% more than 2020). Having a bank account is a prerequisite for a startup to receive VC funds. Mercury can ride with this tide to scale its customer base.

Venture debt

The number of startups taking venture debt has tripled in the last ten years. Mercury is aggressively pursuing venture debt by loaning out $200M in 2022 and $1B in 2023-24. In 2021, ~$47B was raised by startups through venture debt. Even if Mercury gets a small share in this market, venture debt could be a larger product than banking for Mercury.

Banking software for startups offering checking accounts, cards, treasury, and venture debt