Revenue

$486.00M

2024

Valuation

$9.00B

2025

Growth Rate (y/y)

40%

2025

Funding

$1.80B

2025

Revenue

Sacra estimates that N26 hit $486M in revenue in 2024, up 40% from $347M in 2023. The company reached its first quarterly profit in Q3 2024 with net operating income of $3.1M, after achieving monthly profitability starting in June 2024.

N26's revenue growth has been driven by accelerating customer acquisition, with monthly sign-ups exceeding 200,000 and revenue-relevant customers reaching 4.8 million by the end of 2024, up from 4.2 million in 2023. Customer deposits surpassed $11.1B in Q3 2024 for the first time, enabling the bank to expand its treasury and lending activities, with interest revenues now accounting for around 50% of total revenue compared to 40% in 2023.

The company's annual transaction volume is projected to increase 23% to approximately $155B in 2024, with each revenue-relevant customer averaging over $32,000 in transactions. N26's strategic product expansions across investing, crypto trading, joint accounts, and savings products have boosted customer activity metrics while maintaining low customer acquisition costs, with 73% of new customers acquired through word-of-mouth referrals.

Valuation

N26 is valued at $6 billion as of 2023. The company previously reached a peak valuation of $9 billion in 2021 when it generated $208M in revenue, representing a 43.3x revenue multiple during the height of neobank valuations.

The company has raised approximately $1.8 billion in total funding since its founding in 2014. Notable strategic investors have included Allianz SE, though Allianz is currently divesting its position as N26 refocuses on its core European markets following expensive international expansion attempts.

Product

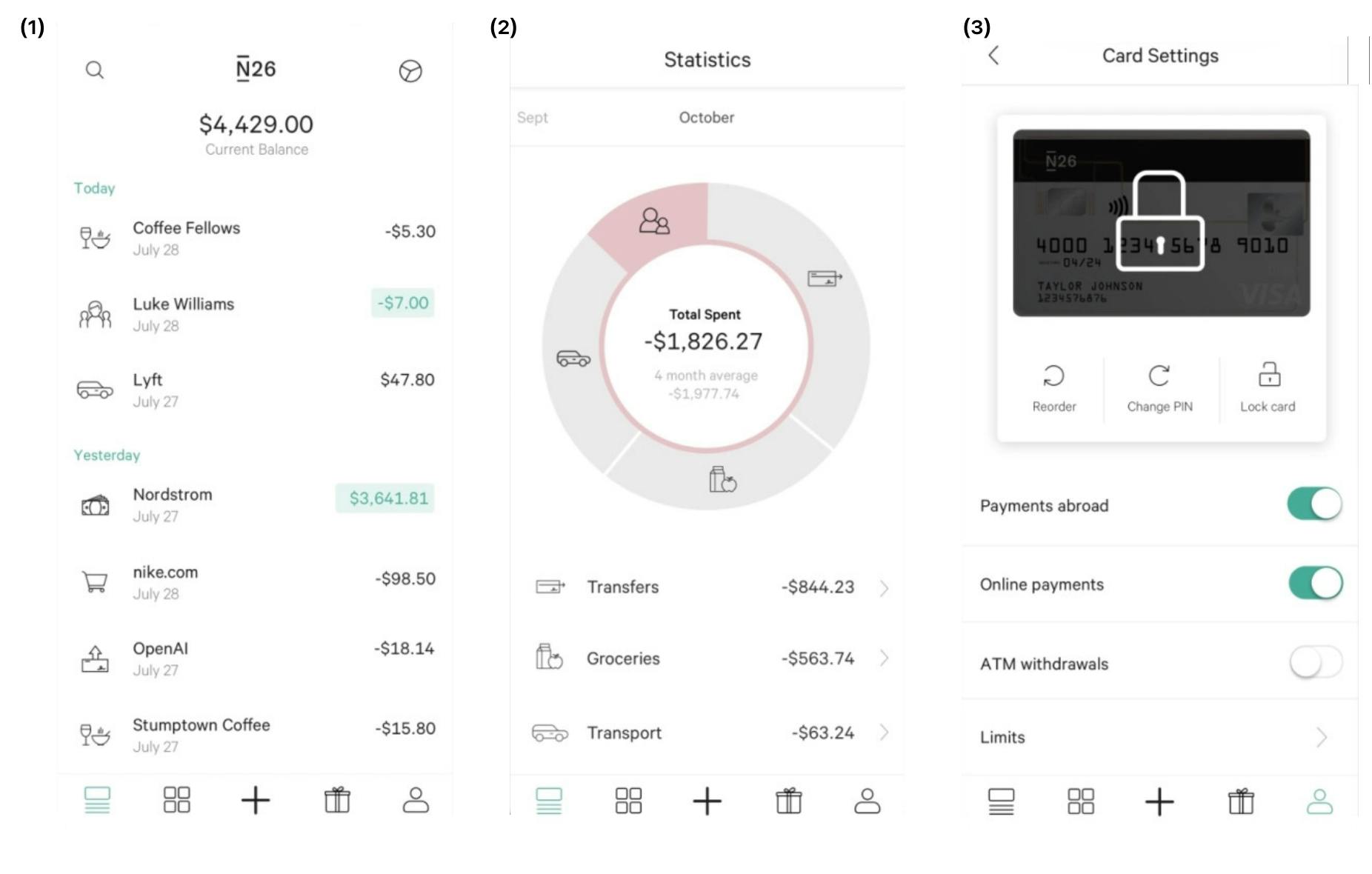

N26 provides a fully-licensed German current account that customers can open in minutes using their smartphone. Users receive an IBAN, SEPA compatibility, and a Mastercard or Visa debit card that works with Apple Pay and Google Pay for instant payments across Europe.

The core experience centers around real-time transaction notifications and spending categorization. When a customer makes a purchase, they immediately see the transaction reflected in their app with automatic categorization for budgeting. Users can create sub-accounts called Spaces for savings goals, with automated transfers and real-time balance tracking.

N26 operates a freemium model where the Standard account includes basic banking features at no cost. Paid tiers at €4.90, €9.90, and €16.90 per month add premium features like additional physical cards, higher ATM withdrawal limits, travel insurance, and cashback rewards.

The platform includes integrated investment options through partnerships. N26 Crypto allows users to buy and sell over 200 cryptocurrencies directly in the app through Bitpanda's infrastructure. N26 Stocks & ETFs enables fractional share trading of 800+ instruments with €1 minimum investments, settling same-day back to the current account through Upvest's API.

Credit products include in-app overdrafts up to €10,000 at 8.9-13.9% APR and installment loans up to €25,000. The company also offers buy-now-pay-later functionality through partner merchants and is developing joint accounts for couples and shared expenses.

Business Model

N26 operates as a vertically integrated digital bank that monetizes through a diversified revenue model combining deposit funding, payment processing, subscription fees, and financial product partnerships. The company holds a full German banking license, enabling it to offer current accounts and accept deposits across the European Union through passporting rights.

The core value delivery mechanism relies on mobile-first user experience and real-time financial data. N26 captures interchange fees of approximately 35 basis points after scheme and processor costs on the €140 billion in annual card volume generated by highly engaged customers who average €29,000 in yearly spending.

The company's funding model has evolved from interchange-dependent to interest-driven. N26 now holds €8-9 billion in customer deposits, generating net interest income through the spread between rates paid to customers and yields earned on treasury investments and lending. This shift enabled profitability as rising rates expanded net interest margins from near-zero to 200+ basis points.

N26's subscription model creates recurring revenue streams while serving as a customer segmentation tool. Approximately 30% of revenue-relevant customers pay for premium features, with higher-tier subscribers exhibiting greater engagement and deposit balances. The tiered pricing structure allows N26 to monetize both price-sensitive users through interchange and affluent customers through subscriptions and wealth products.

The company maintains an asset-light operational model by partnering with specialized providers rather than building everything in-house. Crypto trading runs on Bitpanda's infrastructure, stock trading utilizes Upvest's investment API, and insurance products come through Allianz partnerships. This approach enables rapid feature deployment while keeping development costs lower than full vertical integration.

Competition

The #1 neobank across each European country

Pan-European neobank leaders

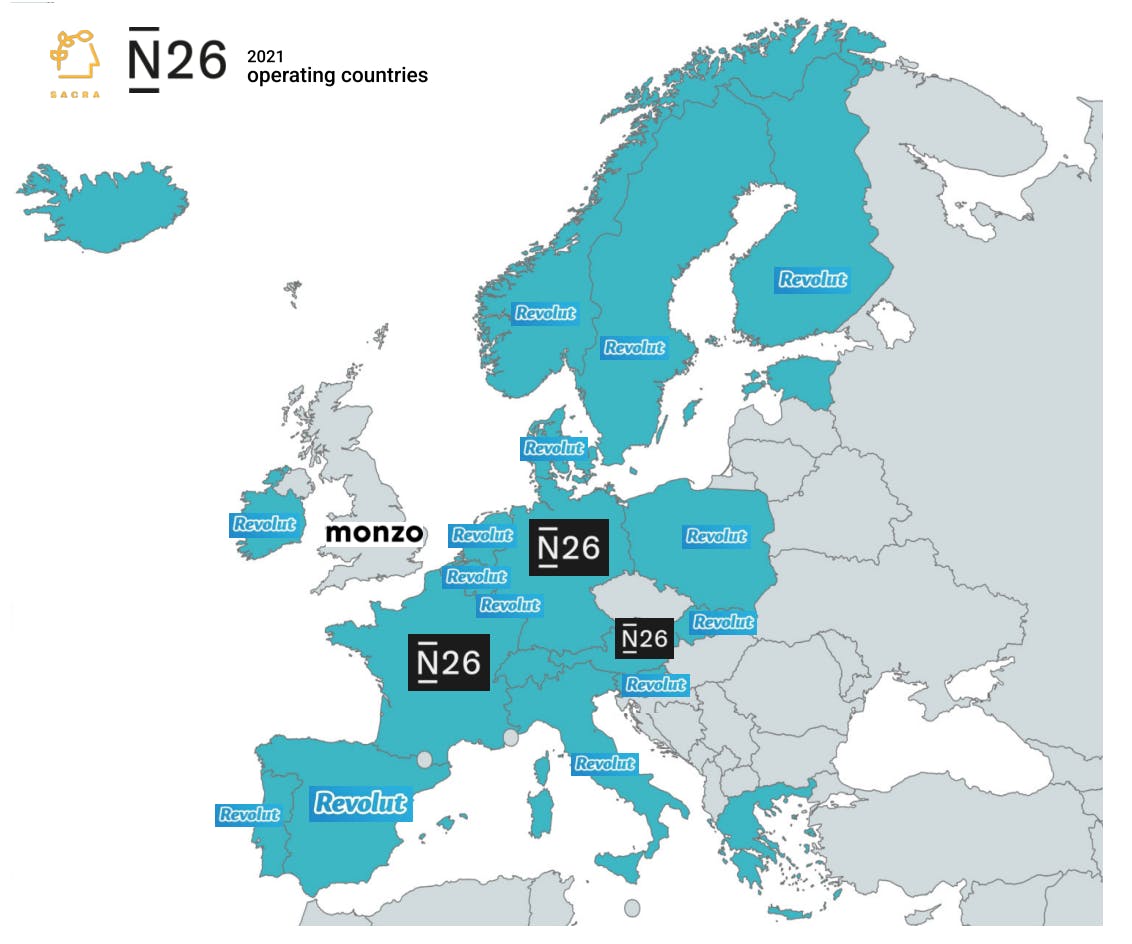

Revolut dominates most European markets where N26 operates, achieving significantly higher scale and ARPU through aggressive geographic expansion and product proliferation. Revolut's €2.3 billion in 2023 revenue dwarfs N26's €328 million, reflecting superior execution in building a financial superapp with crypto, trading, business banking, and international money transfer. N26's more conservative approach has resulted in market share losses to Revolut's broader product suite and marketing spend.

Starling Bank represents an alternative path focused on business banking and banking-as-a-service revenue. While Starling generated €575 million in revenue in 2023, their strategy of selling infrastructure to other fintechs creates a different competitive dynamic than N26's consumer-focused model. Starling's business banking success demonstrates potential upside for N26's planned SME expansion.

Traditional bank digital transformation

Incumbent European banks have substantially improved their digital offerings to compete with neobanks on user experience while leveraging superior balance sheets and regulatory trust. Deutsche Bank's Fyrst, Santander's Openbank, and other traditional bank digital products offer many of the same features as N26 while providing full-service banking relationships and established customer trust.

These incumbents can absorb customer acquisition costs that would be unsustainable for standalone neobanks, while their existing deposit bases provide funding advantages during rate cycles. Traditional banks also avoid the regulatory scrutiny that has constrained N26's growth, as evidenced by BaFin's previous customer acquisition caps on N26's German operations.

Specialized financial services unbundling

Dedicated crypto platforms like Coinbase and Binance provide superior trading experiences compared to N26's white-label crypto integration. Investment platforms such as Trade Republic and Scalable Capital offer more sophisticated trading tools and lower fees than N26's basic stock trading functionality.

Buy-now-pay-later specialists like Klarna and payment companies like Adyen compete for merchant relationships and consumer payment preferences. These focused players often provide better user experiences in their specific verticals, making it difficult for N26 to achieve leadership across all financial services categories within a single app.

TAM expansion

Copy

SME and business banking penetration

N26's planned business banking launch represents its largest near-term TAM expansion opportunity. Small and medium enterprises across Europe generate significantly higher ARPU than consumer customers, with competitors like Revolut Business and Qonto demonstrating €100-150 average annual revenue per business customer potential.

The company already serves over 250,000 retail customers who also own small businesses, providing a natural expansion vector. N26's consumer banking infrastructure can support business features like multi-user access, expense management, and API integrations while leveraging the same mobile-first user experience that differentiates the platform from traditional business banking.

European SME banking remains fragmented with limited digital-native options, particularly in Germany and France where N26 has strong consumer presence. Business customers also exhibit higher deposit balances and lending demand, creating opportunities for N26 to monetize through higher-margin financial products beyond basic payment processing.

Wealth management and long-term savings

N26's expansion into stocks, ETFs, and crypto trading represents the early stages of a broader wealth management strategy. European customers increasingly expect integrated investment options within their primary banking app, creating opportunities to capture assets under management fees and increase customer lifetime value.

The company's roadmap includes robo-advisory services and automated portfolio allocation, potentially generating 10-20 basis points in ongoing AUM fees. Retirement and pension wrapper products could capture long-term savings flows while increasing customer retention through higher switching costs.

European wealth management incumbents typically charge higher fees and provide inferior digital experiences compared to US robo-advisors, suggesting room for N26 to capture market share through better pricing and user experience. The integration with existing banking relationships also provides distribution advantages over standalone investment platforms.

Geographic expansion in underbanked markets

N26's focus on Central and Eastern European expansion targets markets with weaker incumbent digital banking infrastructure and higher growth potential. Countries like Poland, Czech Republic, and Hungary offer less competitive environments than Western Europe while maintaining EU regulatory consistency.

The company's previous expansion failures in the US and Brazil highlight the importance of selecting markets where N26's mobile-first approach provides clear differentiation versus local incumbents. Eastern European markets often lack strong neobank competitors while maintaining sufficient smartphone penetration and regulatory frameworks to support digital banking adoption.

Latin American expansion remains a longer-term opportunity following the successful examples of Nubank in Brazil and Kapital in Mexico. However, N26's strategy now emphasizes depth over breadth, focusing on maximizing revenue per customer in existing markets rather than aggressive geographic expansion that proved costly in previous attempts.

News

DISCLAIMERS

This report is for information purposes only and is not to be used or considered as an offer or the solicitation of an offer to sell or to buy or subscribe for securities or other financial instruments. Nothing in this report constitutes investment, legal, accounting or tax advice or a representation that any investment or strategy is suitable or appropriate to your individual circumstances or otherwise constitutes a personal trade recommendation to you.

This research report has been prepared solely by Sacra and should not be considered a product of any person or entity that makes such report available, if any.

Information and opinions presented in the sections of the report were obtained or derived from sources Sacra believes are reliable, but Sacra makes no representation as to their accuracy or completeness. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information, opinions and estimates contained in this report reflect a determination at its original date of publication by Sacra and are subject to change without notice.

Sacra accepts no liability for loss arising from the use of the material presented in this report, except that this exclusion of liability does not apply to the extent that liability arises under specific statutes or regulations applicable to Sacra. Sacra may have issued, and may in the future issue, other reports that are inconsistent with, and reach different conclusions from, the information presented in this report. Those reports reflect different assumptions, views and analytical methods of the analysts who prepared them and Sacra is under no obligation to ensure that such other reports are brought to the attention of any recipient of this report.

All rights reserved. All material presented in this report, unless specifically indicated otherwise is under copyright to Sacra. Sacra reserves any and all intellectual property rights in the report. All trademarks, service marks and logos used in this report are trademarks or service marks or registered trademarks or service marks of Sacra. Any modification, copying, displaying, distributing, transmitting, publishing, licensing, creating derivative works from, or selling any report is strictly prohibited. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express written permission of Sacra. Any unauthorized duplication, redistribution or disclosure of this report will result in prosecution.