Revenue

$1.50B

2024

Valuation

$5.50B

2024

Growth Rate (y/y)

128%

2024

Funding

$27.00M

2024

Revenue

Sacra estimates that Kraken hit $1.5 billion in revenue for 2024, growing 128% year-over-year. This strong performance reflects the company's resilience and ability to capitalize on market opportunities, with total trading volume reaching $665 billion in 2024.

Kraken primarily monetizes on transaction volume, with total trading volume reaching $665 billion in 2024, representing a significant recovery from previous years' volumes of $268 billion in 2023 and $310 billion in 2022.

In 2024, client assets on platform grew to $42.8 billion, while adjusted EBITDA grew to $380 million.

This growth was supported by continued expansion of the platform's user base, which reached 2.5 million funded accounts by year-end. Kraken now says it handles over 40% of global stable-to-fiat trading volume among major centralized exchanges, cementing its position as a leading fiat on-ramp in the cryptocurrency market.

Valuation

Based on their most recent valuation of $5.5B, set in their 2020 Series B, and their $954M in revenue in 2020, Kraken traded at a 5.8x multiple. The company has raised $27M in total primary funding.

Product

Founded in 2011, Kraken launched its crypto exchange in 2013, finding product-market fit as the only place to buy and sell Bitcoin with euros—revenue grew from about $160M in 2017 to $2B in 2021 as total Bitcoin trading volume rose from $53B to $625B.

The exchange officially launched to the public in September 2013, initially offering trading for Bitcoin, Litecoin, euro, and US dollar.

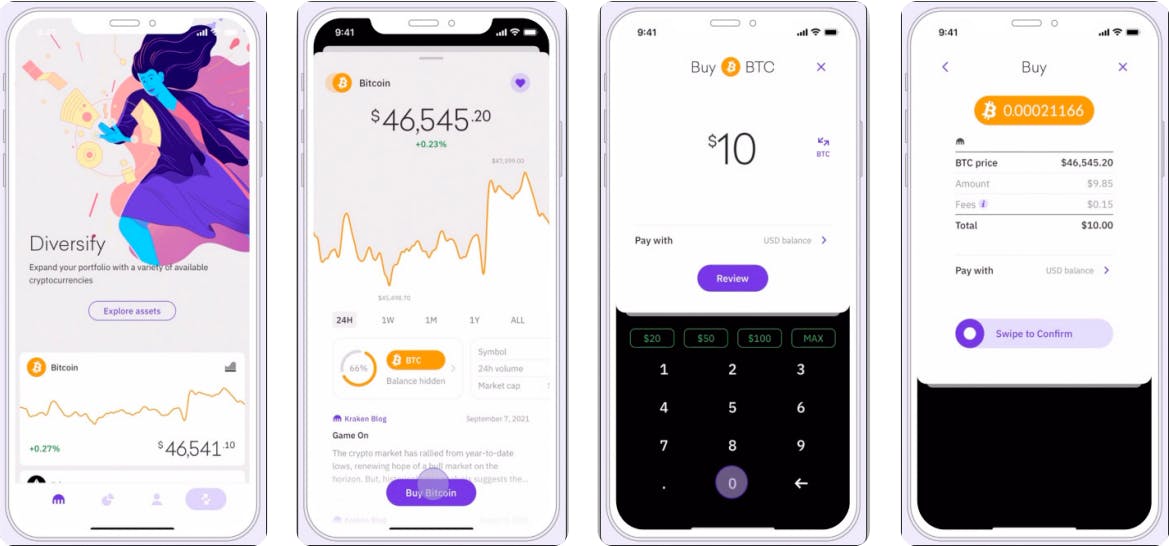

Kraken's consumer experience on iOS enables users to buy from across 70+ cryptocurrencies with a minimum deposit of $10.

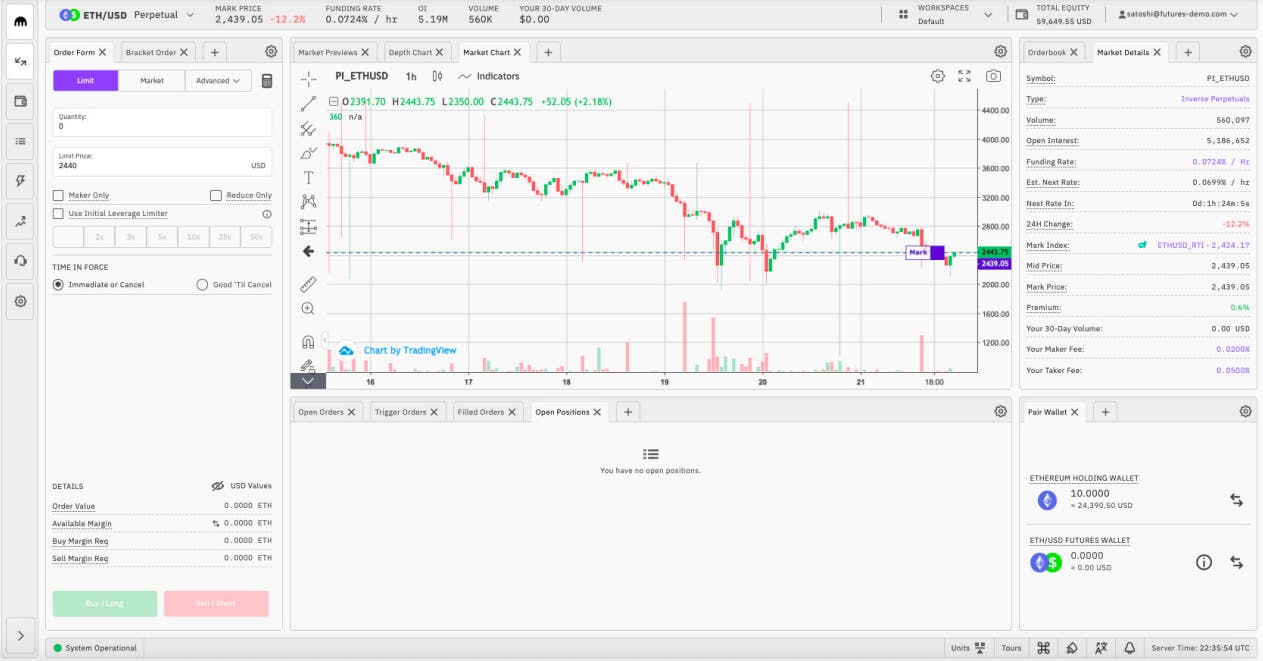

On the web, Kraken offers a fully-featured order book and trading interface that can be customized by the user.

Kraken positions itself as a secure and regulation-compliant exchange. It holds 95% of deposits in air-gapped, geo-distributed cold storage and has not faced any hacking/coin theft incidents since its launch. It is registered with key regulatory bodies such as FinCEN (US), FINTRAC (Canada), FCA (UK), and AUSTRAC (Australia). For comparison, Binance (largest crypto exchange by volume) doesn’t provide any details on customer deposit safety measures. It had a large-scale security breach in 2019, resulting in the theft of $40 million in Bitcoin.

Kraken acquired a Special Purpose Depository Institution Charter from the state of Wyoming in 2020, and as a result, plans to begin bank operations for digital assets in 2022. This is essential to Kraken’s vision of being the most trusted bridge between the crypto economy and the existing financial system—acquiring an SPDIC means that Kraken can offer new products such as custodial services, US dollar deposits, debit card, salary accounts, and stock trading.

The license does come with a few restrictions—most notably, that Kraken Bank becomes a ‘custody bank’ and cannot use its crypto deposits for lending. Also, it is required to hold reserves backing 100% of customer deposits in the form of US Treasury securities, corporate debt, and other investment-grade debt instruments.

The exchange serves over 9 million users across 190+ countries. While Europe remains Kraken's largest market, it has expanded significantly in North America and is growing in regions like Japan, Australia, and the UAE.

Business Model

Kraken's core business model revolves around taking a percentage fee on each trade executed on its platform.

For spot trading on Kraken Pro, maker fees range from 0.25% for low volume traders down to 0.06% for high volume traders, while taker fees range from 0.40% to 0.20%.

The basic exchange charges higher fees of 0.9% for stablecoin trades and 1.5% for other crypto assets.

Beyond trading fees, Kraken has diversified its revenue streams through several additional products and services.

The company charges a 3.75% fee plus a small fixed amount for credit/debit card purchases.

It also generates income from margin trading fees, futures trading fees, and staking rewards. Kraken's NFT marketplace takes a 2% cut of transactions.

A key strategy for Kraken has been expanding its fiat currency support, allowing it to serve as an important fiat on-ramp in multiple regions. The exchange supports 7 fiat currencies including USD, EUR, GBP, and JPY. This has helped Kraken build a strong presence in Europe, where it commands over 50% market share in EUR trading.

Competition

Global Exchanges

In the global exchange space, Kraken's primary competitors are Coinbase and Binance. Coinbase, a publicly-traded company with an $18 billion market cap, has a strong presence in the U.S. market and offers a user-friendly platform for retail investors.

Binance, the largest crypto exchange by trading volume, has a $60 billion valuation and processes four times the trading volume of Coinbase.

Kraken differentiates itself through its focus on security, having never been hacked, and its transparent Proof-of-Reserve system that verifies client asset holdings. Kraken also emphasizes its role as a bridge between traditional finance and crypto, supporting seven fiat currencies compared to many competitors' more limited fiat options.

Regional Players

Kraken has a strong presence in Europe, where it was an early mover in offering Bitcoin trading with euros and British pounds. The company has increased its share of EUR spot markets from 35% to 53% over the past year.

In this category, Kraken competes with regional exchanges like Bitstamp and BitPanda. Kraken's advantage lies in its longer operating history, broader range of supported cryptocurrencies (215 coins and 644 trading pairs), and more advanced trading features like margin trading with up to 5x leverage on certain pairs.

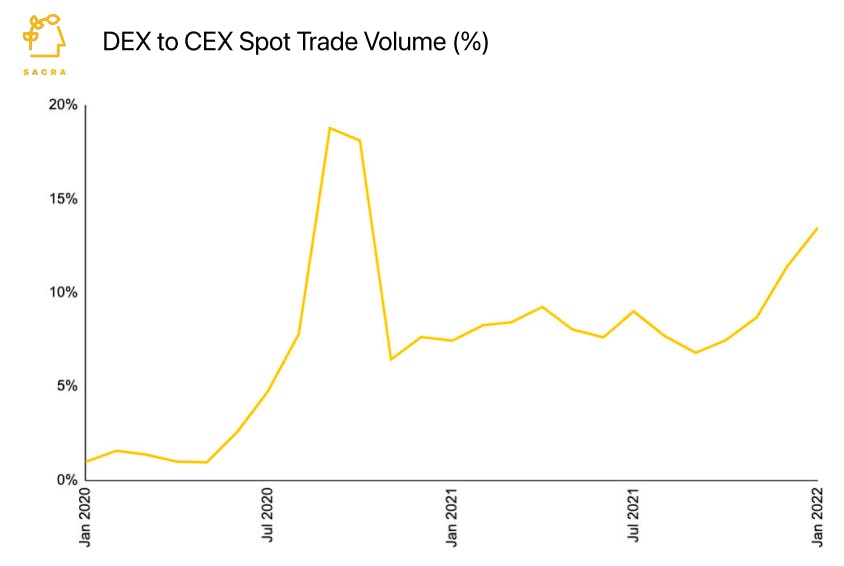

Decentralized Exchanges

While not necessarily direct competitors, decentralized exchanges (DEXs) like Uniswap and SushiSwap represent a growing alternative to centralized platforms like Kraken. A DEX operates without an intermediary for clearing transactions and relies on self-executing smart contracts for trading. A DEX enables instantaneous trades at a lower cost compared to centralized exchanges.

TAM Expansion

Kraken is indexed on the upside of the next crypto boom with its counter-positioning against the legally imperiled Binance as a safe, “boring” exchange that custodies customer funds rather than launching exotic products like exchange stablecoins.

Financial Services

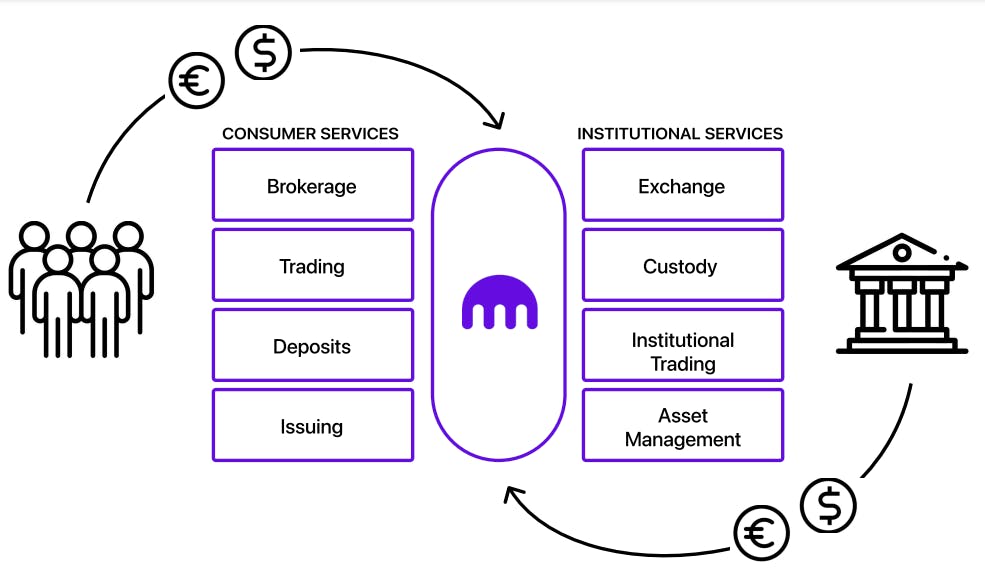

The financial services world is broken into various silos that do not play well with each other—lending, brokerage, crypto, banking, among others. This requires the consumer to move across apps/platforms for different use cases. However, the consumer doesn’t want to be bothered by the back-end infrastructure and prefers to access all financial products in a seamless experience within one app.

Being an SPDI charter bank allows Kraken to build a financial services app that solves this problem as the charter brings many financial services silos under a single regulatory umbrella. Kraken can provide various services—cards, bill payment, salary payment, deposits, trading, etc. within a single app without having the user jump across multiple apps.

Kraken's advantage over other players in the crypto ecosystem attempting to solve this problem is that the charter gives Kraken access to the Fed’s payment rails. So, Kraken can do all of this in-house and at a lower cost than other crypto ecosystem players.

Liquidity

Kraken now can build a crypto finance house with both consumer and institutional wings a la JP Morgan, addressing the massive liquidity gap in the crypto market today. They can expand their consumer offering, and on the institutional side, manage assets and conduct custodial and other kinds of financial activities. These new products mean the potential for massive new inflows of capital. Kraken could also use that capital to provide liquidity to the institutions, crypto companies, and miners that need liquidity—to run their book on leverage, to take out loans against their assets, or to buy hardware without selling equity, respectively—but can’t get it from the traditional financial ecosystem today.

To keep user capital coming in, Kraken must continue to expand its range of services to stay competitive with exchanges like Coinbase and other emerging services. The exchange business model is quickly becoming commoditized, with players like Robinhood and Block building easy on-ramps into crypto with millions of on-boarded users.

To continue to strengthen Kraken’s value proposition as a place to hold funds, Kraken built a staking business, which grew to $16 billion in transaction volume at the end of 2021 (950% growth year-over-year) and acquired the non-custodial staking platform Staked to add to their staking portfolio in December. They also announced the launch of an NFT marketplace that would allow users to borrow against their NFTs, similar to what DeFi platforms like Nexo and Arcade offer.

Risks

1. Regulatory Uncertainty: As a US-based crypto exchange, Kraken faces significant regulatory risk, especially given recent SEC actions against the company. The SEC's allegations that certain crypto assets are securities could force Kraken to delist popular tokens or face hefty fines, potentially driving users to offshore exchanges. While Kraken is fighting the latest SEC complaint, prolonged legal battles could drain resources and damage its reputation.

2. Market Share Erosion: Despite recent gains, Kraken's market share remains vulnerable. Its 21% share of USD deposit-supporting exchanges is still less than rivals like Coinbase. As the crypto market matures, larger players or new entrants with superior technology could erode Kraken's position, especially if they offer more competitive fees or innovative features.

3. Overreliance on Trading Revenue: Kraken's revenue is heavily dependent on trading volumes, which are highly cyclical in crypto markets. The company's estimated revenue drop from $1.35B in 2021 to $880M in 2023 highlights this vulnerability. While Kraken is diversifying into areas like staking and futures, it may struggle to develop significant alternative revenue streams quickly enough to offset potential prolonged downturns in trading activity.

Funding Rounds

|

|

||||||

|

||||||

|

|

||||||

|

||||||

|

|

||||||

|

||||||

| View the source Certificate of Incorporation copy. |

News

DISCLAIMERS

This report is for information purposes only and is not to be used or considered as an offer or the solicitation of an offer to sell or to buy or subscribe for securities or other financial instruments. Nothing in this report constitutes investment, legal, accounting or tax advice or a representation that any investment or strategy is suitable or appropriate to your individual circumstances or otherwise constitutes a personal trade recommendation to you.

This research report has been prepared solely by Sacra and should not be considered a product of any person or entity that makes such report available, if any.

Information and opinions presented in the sections of the report were obtained or derived from sources Sacra believes are reliable, but Sacra makes no representation as to their accuracy or completeness. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information, opinions and estimates contained in this report reflect a determination at its original date of publication by Sacra and are subject to change without notice.

Sacra accepts no liability for loss arising from the use of the material presented in this report, except that this exclusion of liability does not apply to the extent that liability arises under specific statutes or regulations applicable to Sacra. Sacra may have issued, and may in the future issue, other reports that are inconsistent with, and reach different conclusions from, the information presented in this report. Those reports reflect different assumptions, views and analytical methods of the analysts who prepared them and Sacra is under no obligation to ensure that such other reports are brought to the attention of any recipient of this report.

All rights reserved. All material presented in this report, unless specifically indicated otherwise is under copyright to Sacra. Sacra reserves any and all intellectual property rights in the report. All trademarks, service marks and logos used in this report are trademarks or service marks or registered trademarks or service marks of Sacra. Any modification, copying, displaying, distributing, transmitting, publishing, licensing, creating derivative works from, or selling any report is strictly prohibited. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express written permission of Sacra. Any unauthorized duplication, redistribution or disclosure of this report will result in prosecution.