Revenue

$23.10M

2021

Valuation

$500.00M

2022

Funding

$199.50M

2022

Revenue

Bloom & Wild generated $150M in revenue in 2024, down from its peak of $191M in 2021, as the company prioritized profitability over growth amid challenging macroeconomic conditions. The business successfully turned profitable with $5.6M in adjusted EBITDA, an improvement of $12M year-over-year, driven by tighter cost controls and reduced marketing spend.

The company's growth story traces back to the COVID era, when revenue surged from $23M in 2018 to $191M in 2021 as consumers shifted to online flower delivery while traditional retail stores remained closed.

Over 90% of orders came from long-distance gifting, where senders and recipients were in different locations. This expansion was further accelerated by strategic acquisitions of Bloomon (Netherlands) and Bergamotte (France).

While the 2024 revenue decline was heavily weighted to the first half of the year, momentum recovered by March 2024. The company's refined focus on customer retention over acquisition has improved unit economics, particularly in key markets like Germany where they're seeing ~50% growth.

The business has also diversified beyond their core flower delivery, expanding into non-flower gifting categories across eight European markets, with current trading showing promising growth across both segments.

Valuation

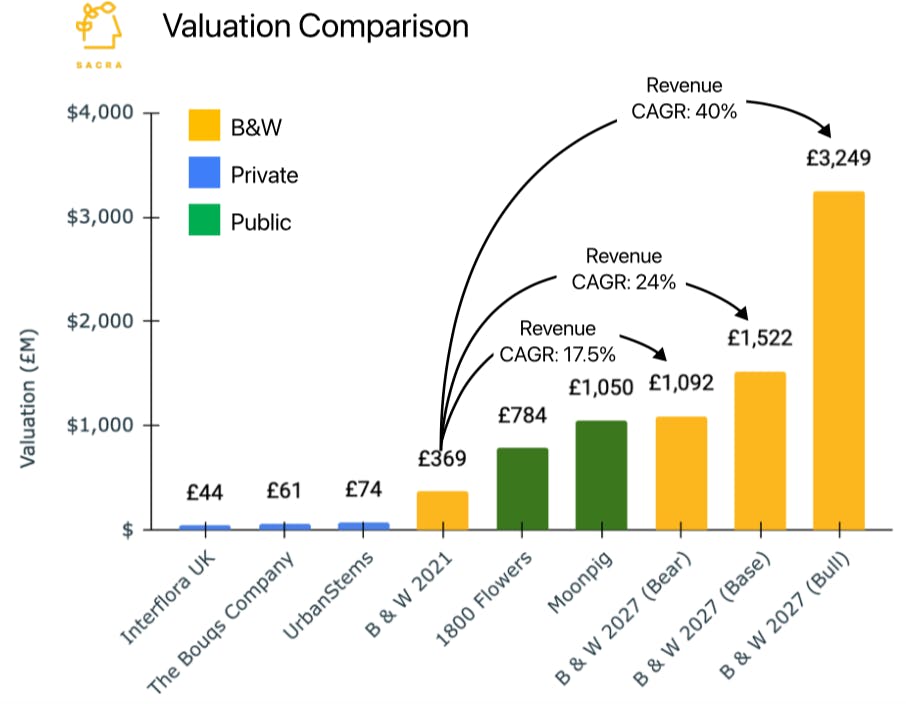

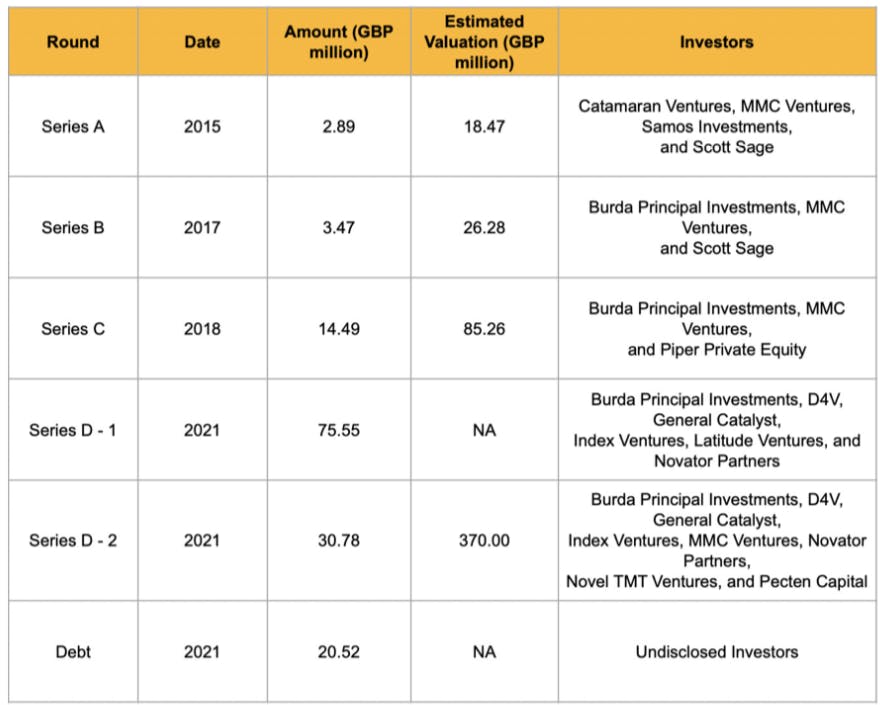

Bloom & Wild raised $102M in a Series D round led by General Catalyst in 2021, reaching an approximate $500M valuation. With $191M in revenue for 2021, this implies a 2.6x revenue multiple.

Bloom & Wild has raised from multiple prominent investors including Index Ventures, Novator, Latitude Ventures, D4 Ventures, and Burda Principal Investments.

Product

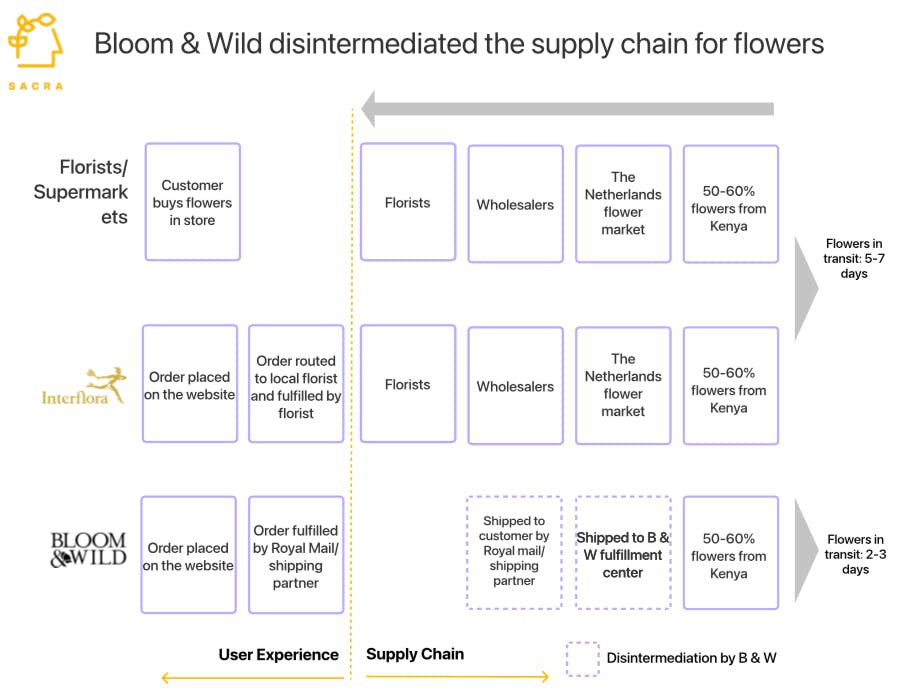

B&W innovated across both the supply chain and the user experience:

From the farm to the mailbox: B&W sources flowers directly from growers, unlike other flower delivery companies (online and physical). It receives the flowers at its fulfilment centers and despatches these to customers through its shipping partners. This reduces costs, transit time, and ensures customers get fresh flowers.

Product innovation: B&W is the first company in Europe to launch letterbox flowers where flower buds are placed in a slim box that can be slid through the recipient’s letterbox. This solves a key problem of missed delivery due to the receiver not being home. The boxed flowers are shipped through Royal Mail/shipping partners with tracking and an improved delivery experience.

Better mobile UX: B&W invested significantly in creating an in-house tech team to build a smooth mobile ordering experience. As millennials and Gen Z prefer ecommerce transactions on mobile, this strategy differentiated them from other online flower platforms with sub-optimal mobile user experience. In 2018, ~50% of orders came from their app, and ~62% of traffic came from mobile.

Demand prediction technology: B&W uses advanced forecast models and prediction algorithms to place orders with growers, reducing wastage, and transit time of flowers.

Competition

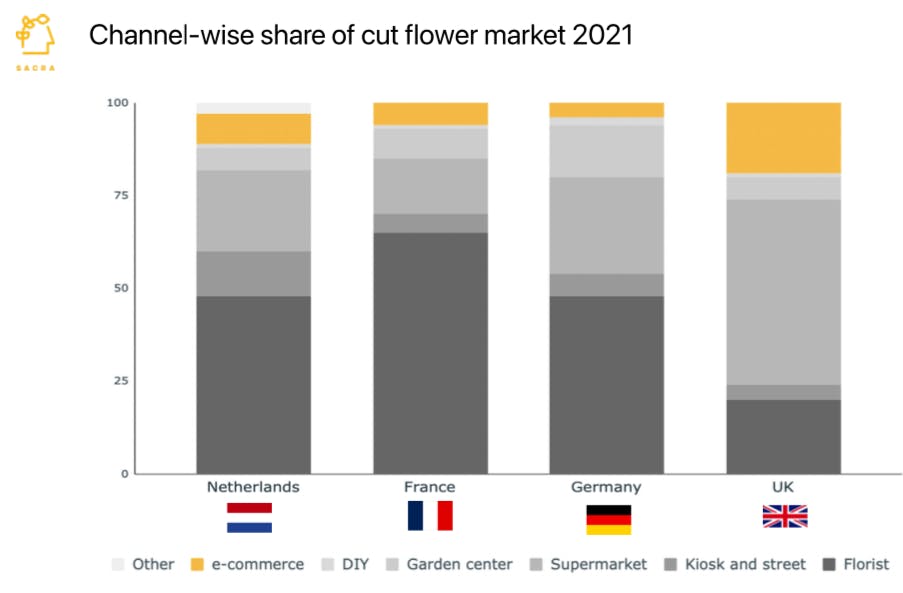

B&W competes for wallet share with physical retail channels such as florists, supermarkets, and ecommerce companies such as Interflora. In the UK, B&W’s primary competition is supermarkets with ~50% market share of cut flowers. However, in France, it competes with florists with ~65% share.

The share of ecommerce in flower delivery in Europe varies from ~5% (Germany) to ~20% (UK). In the ecommerce category, Interflora was the largest player in the UK till 2020, with revenue of £102 million. However, in 2021, B&W overtook Interflora as the largest ecommerce player. B&W benefitted due to its centralized supply chain that does not rely on local florists, many of who suffered due to COVID-related restrictions, for order fulfilment.

Over the next several years, ecommerce’s share of the flower delivery market is expected to continue to grow, mainly at the expense of local florists.

TAM Expansion

There are two main upside cases for B&W:

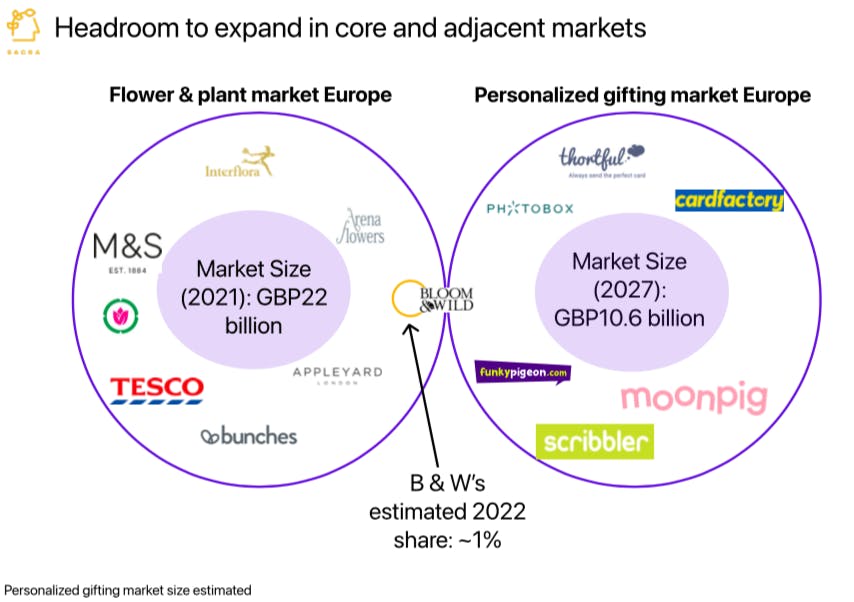

Deeper penetration in the flower market: B&W’s share in the flower market is ~1% which means there’s a lot of headroom for growth. It is experimenting with brick & mortar channel through a partnership with Sainsbury’s to expand its user base beyond ecommerce shoppers in the UK. Another avenue for growth is corporate flower gifting, with companies sending flowers to employees, clients, and business associates. B&W already has companies such as Tesla, UBS, and Meta as its corporate customers.

Shift to adjacent market: Personalized gifting is a large market in Europe, expected to grow to ~£11 billion by 2027. The recent entry of Moonpig, a leading European personalized gifting player in the flower market, highlights the commonalities between the two markets. B&W can leverage its supply chain excellence and technology such as predictive models to enter this adjacent market.

Risks

Post-COVID return to normalcy: COVID-19-related lockdown measures fuelled B&W’s growth in 2021. As the pandemic eases out, B&W may struggle to grow its revenue at last year’s pace. Shoppers could prefer to support local businesses such as florists and high street shops that have struggled due to COVID-related restrictions, potentially impacting short-term revenue.

Managing international acquisitions: B&W recently acquired two of its competitors - Bloomon (The Netherlands) and Bergamotte (France). As it has no prior history of completing large-scale acquisitions successfully, it may struggle to integrate the operations and people from these companies. This could limit the revenue improvement and operational efficiencies that B&W may be hoping to achieve from these acquisitions.

Supply chain: B&W sources ~60% of its flowers from Kenya, increasing its exposure to any geopolitical or air cargo issues that can disrupt its supply chain. Most of its competitors source flowers from The Netherlands flower market and aren’t directly exposed to this risk.

Comps

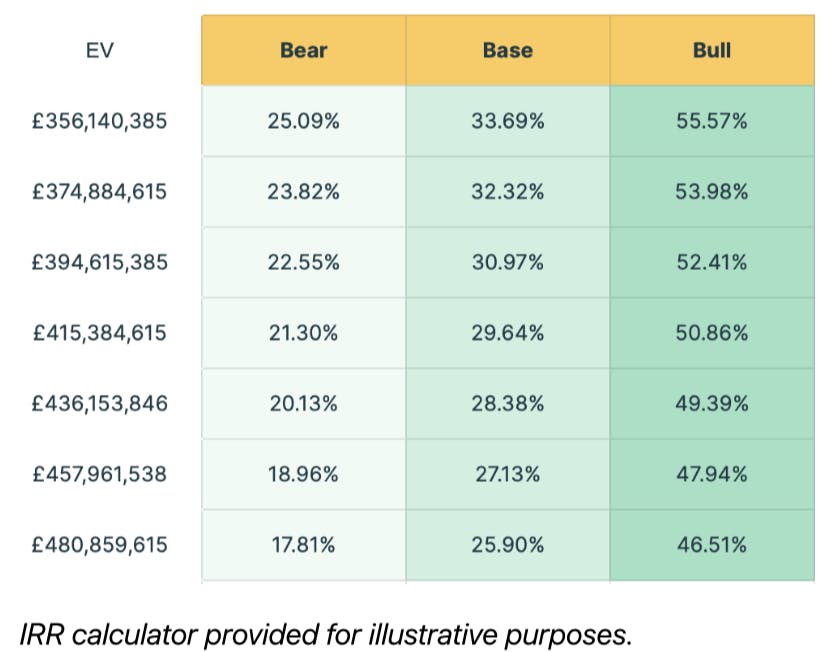

The European flower market is extremely fragmented and no player has market share of more than 1%. Thus, we look at Bloom & Wild’s future growth in context of its pre-pandemic growth. Our base case estimates revenue to grow at a CAGR of 24% (~1/3rd of its average pre-pandemic growth rate) to reach £514 million in 2027. The growth is driven by the increase in ecommerce share in the flower market and above-average synergies from the acquisition of Bloomon and Bergamotte.

For the bear case, we estimate Bloom & Wild’s revenue to grow substantially slower than pre-pandemic growth at ~17.5% and revenue stagnation at £369 million. Our bull case assumes high synergies from Bloomon and Bergamotte and an accelerated shift to ecommerce even post-COVID.

We estimate Bloom & Wild to grow at a CAGR of ~40% in our bull case (~2/3rd of its average pre-pandemic growth rate) to reach revenue of ~£1 billion in 2027. We expect B&W to maintain a valuation/revenue multiple of ~3X.

Fundraising

News

DISCLAIMERS

This report is for information purposes only and is not to be used or considered as an offer or the solicitation of an offer to sell or to buy or subscribe for securities or other financial instruments. Nothing in this report constitutes investment, legal, accounting or tax advice or a representation that any investment or strategy is suitable or appropriate to your individual circumstances or otherwise constitutes a personal trade recommendation to you.

This research report has been prepared solely by Sacra and should not be considered a product of any person or entity that makes such report available, if any.

Information and opinions presented in the sections of the report were obtained or derived from sources Sacra believes are reliable, but Sacra makes no representation as to their accuracy or completeness. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information, opinions and estimates contained in this report reflect a determination at its original date of publication by Sacra and are subject to change without notice.

Sacra accepts no liability for loss arising from the use of the material presented in this report, except that this exclusion of liability does not apply to the extent that liability arises under specific statutes or regulations applicable to Sacra. Sacra may have issued, and may in the future issue, other reports that are inconsistent with, and reach different conclusions from, the information presented in this report. Those reports reflect different assumptions, views and analytical methods of the analysts who prepared them and Sacra is under no obligation to ensure that such other reports are brought to the attention of any recipient of this report.

All rights reserved. All material presented in this report, unless specifically indicated otherwise is under copyright to Sacra. Sacra reserves any and all intellectual property rights in the report. All trademarks, service marks and logos used in this report are trademarks or service marks or registered trademarks or service marks of Sacra. Any modification, copying, displaying, distributing, transmitting, publishing, licensing, creating derivative works from, or selling any report is strictly prohibited. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express written permission of Sacra. Any unauthorized duplication, redistribution or disclosure of this report will result in prosecution.